Monitor performance and risk measures across the entire S&P 500

The S&P 500 Tables Screening dashboard allows investors to monitor performance across the entire index by ranking returns over various lookback periods, such as 30, 60, and 90 trading days. By analyzing these rankings, traders can easily identify momentum leaders and laggards in the S&P 500, facilitating informed investment decisions.

The Sharpe ratio included in the S&P 500 Tables Screening dashboard measures risk-adjusted returns for each stock over different trading horizons. By comparing these ratios, investors can evaluate which stocks are delivering the best performance relative to their risk, helping to optimize their equity market strategies.

The RSI-style breadth metric in the S&P 500 Tables Screening dashboard calculates the percentage of trading days with positive returns for each stock. This metric provides insights into market momentum and can help investors gauge the overall strength or weakness of stocks within the S&P 500.

This dashboard provides S&P 500 stock screening tables built from daily price data for every index constituent. It ranks returns across multiple lookback windows (such as 30, 60, 90 and 252 trading days) to compare short- and medium-term performance. It also computes Sharpe ratios over the same horizons to evaluate risk-adjusted returns, and includes an RSI-style breadth metric based on the percentage of days with positive returns. Tables are designed for fast cross-sectional comparison to identify momentum leaders, laggards and changes in risk-adjusted performance. Use it to scan the entire S&P 500 efficiently and export the underlying data for deeper analysis.

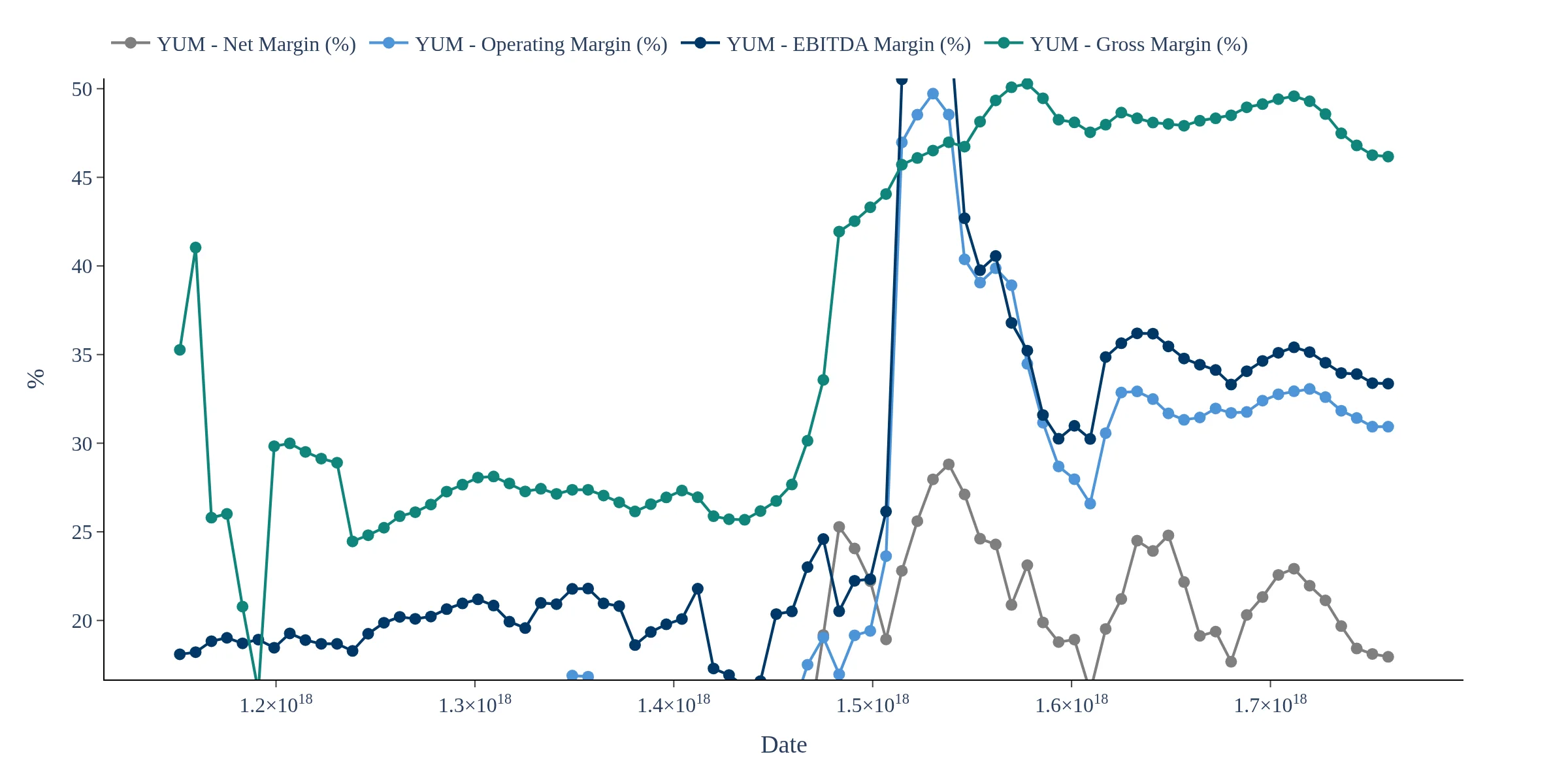

Track quarterly financials for all the stocks in the S&P 500 - Interactive charts with downloadable data

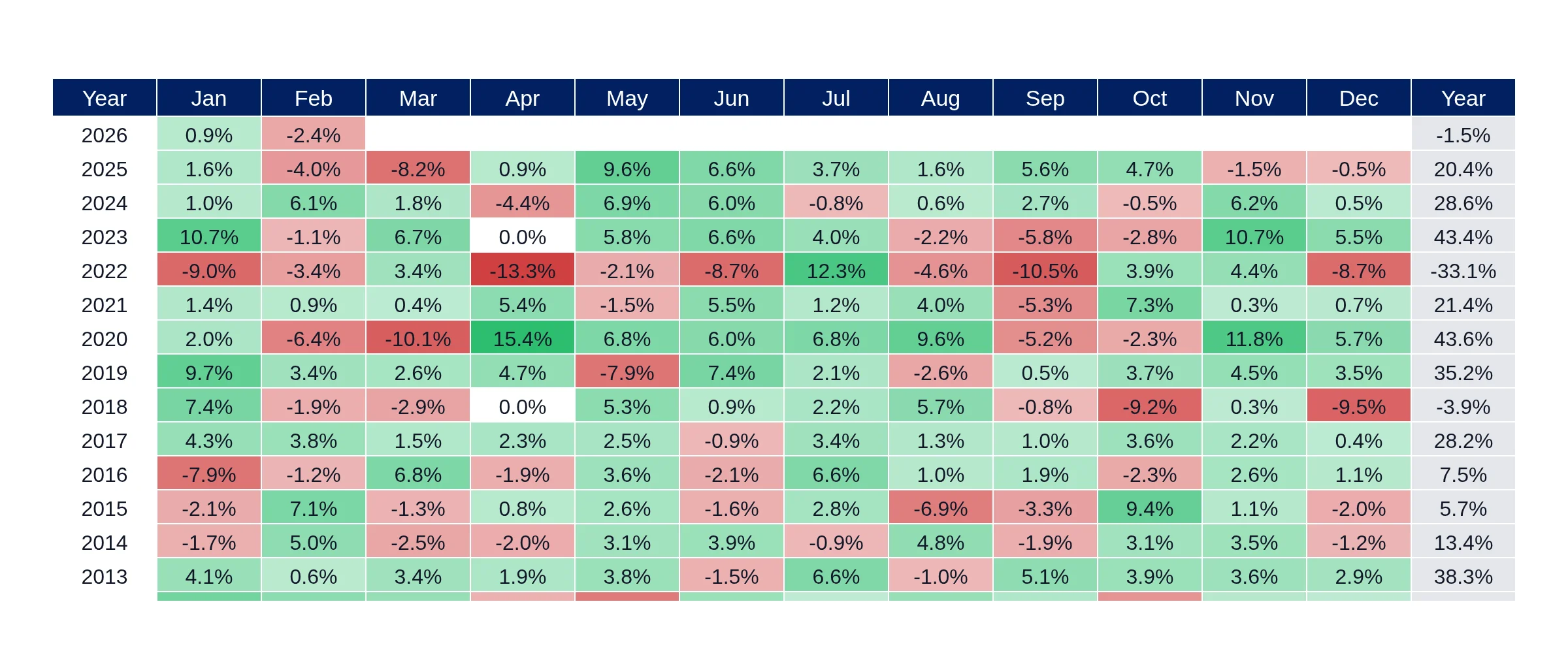

Track price and risk metrics for all the companies inside the S&P 500

Track Nasdaq Index returns like no other tool does