Dashboard consolidating backtest and analysis on a vol-weighted portfolio of Bitcoin, S&P 500 and Gold.

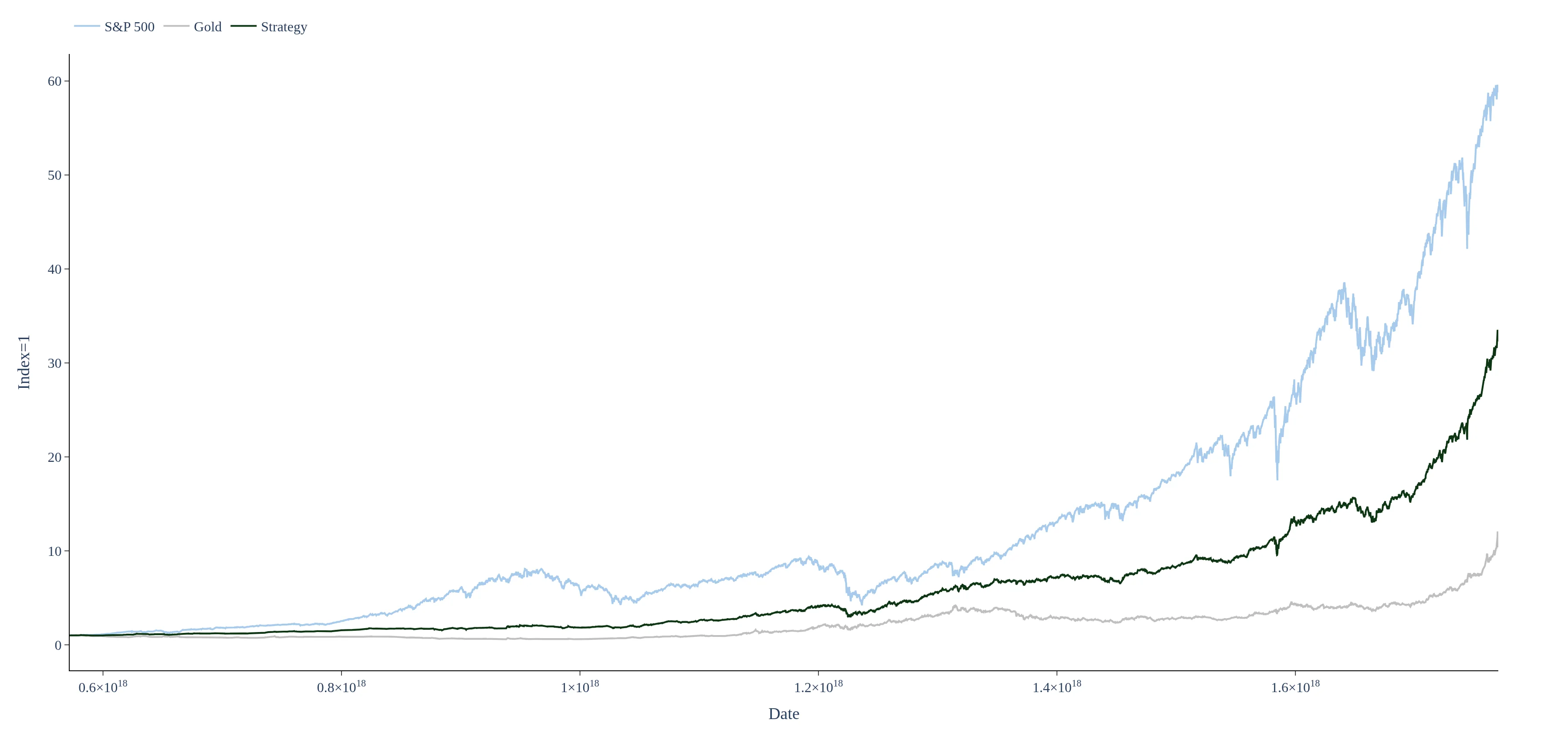

The Bitcoin + S&P 500 + Gold EWMA Volatility Adjusted Portfolio manages risk by using Exponentially Weighted Moving Average (EWMA) volatility to size each asset's allocation. This methodology targets a similar risk contribution from each asset, allowing the portfolio to reduce exposure to high-volatility assets like Bitcoin during turbulent market conditions while increasing allocation to lower-volatility assets such as Gold and equities.

The dashboard provides performance metrics as a normalized index in USD, showcasing both monthly and annual returns of the Bitcoin + S&P 500 + Gold EWMA Volatility Adjusted Portfolio. Additionally, it compares the portfolio's performance against a US T-Bill proxy, allowing investors to evaluate its effectiveness relative to a cash benchmark.

You can analyze different market cycles using the time-window buttons available on the dashboard, which allow you to evaluate regime behavior, drawdowns, and diversification benefits across various market conditions. This feature helps investors understand how the volatility-adjusted portfolio performs during different economic environments, enhancing strategic decision-making.

This dashboard backtests a volatility-adjusted portfolio combining Bitcoin, the S&P 500 and Gold, sized using EWMA volatility (here shown with a 30-day vol setting). Daily returns are used to estimate rolling EWMA vol for each asset, then portfolio weights are scaled so each asset targets a similar risk contribution. The result is a simple risk-balanced allocation that tends to de-risk high-vol regimes (often Bitcoin) and lean more on lower-vol assets (often equities or gold). Performance is shown as a normalized index in USD and compared to a US T-Bill proxy as a cash benchmark. Use the time-window buttons to evaluate regime behavior, drawdowns and diversification benefits across different market cycles.

Get insights into how being long the S&P 500 and Gold on a vol adjusted basis is performing

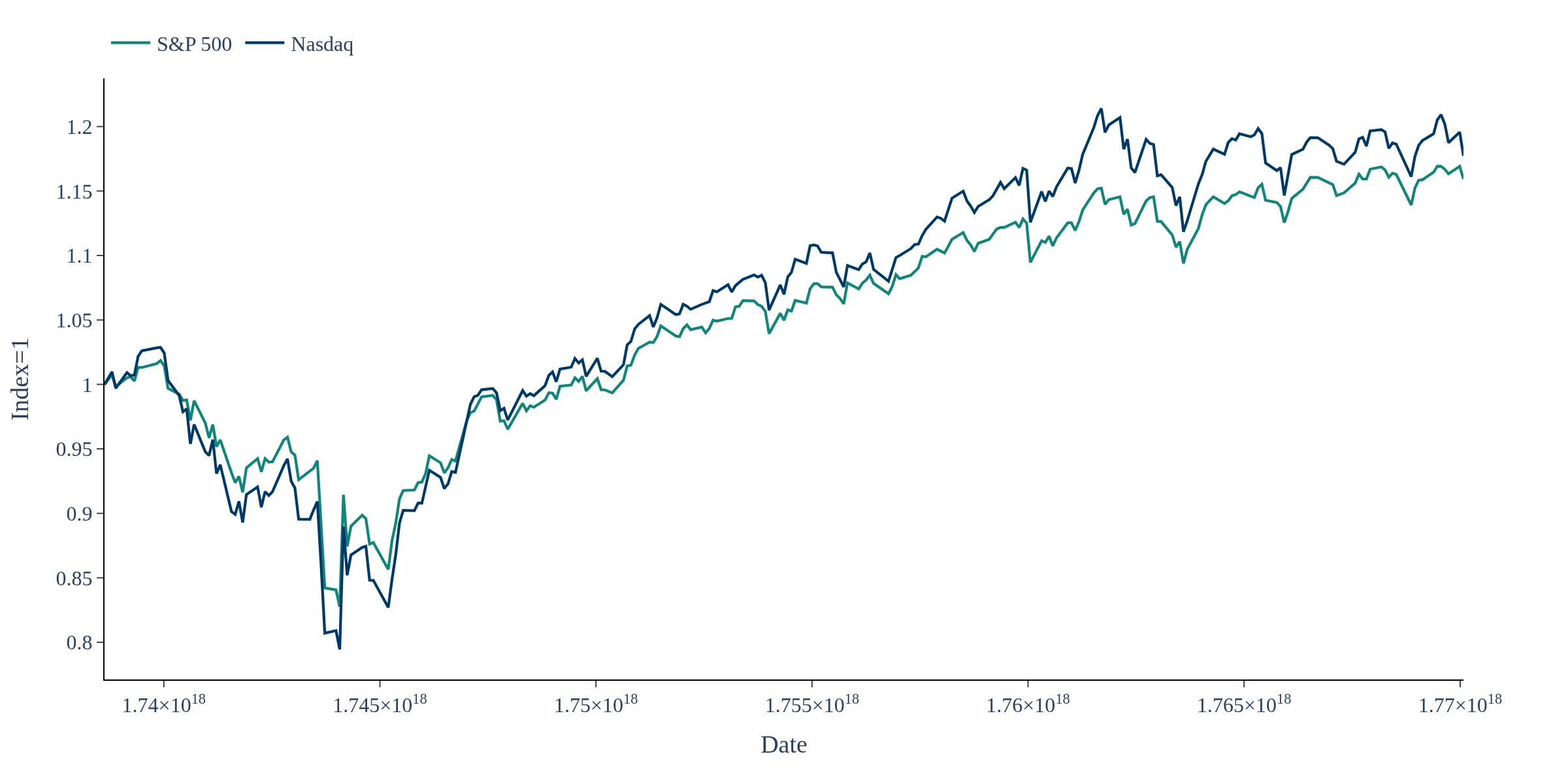

Track how are US Equities are behaving

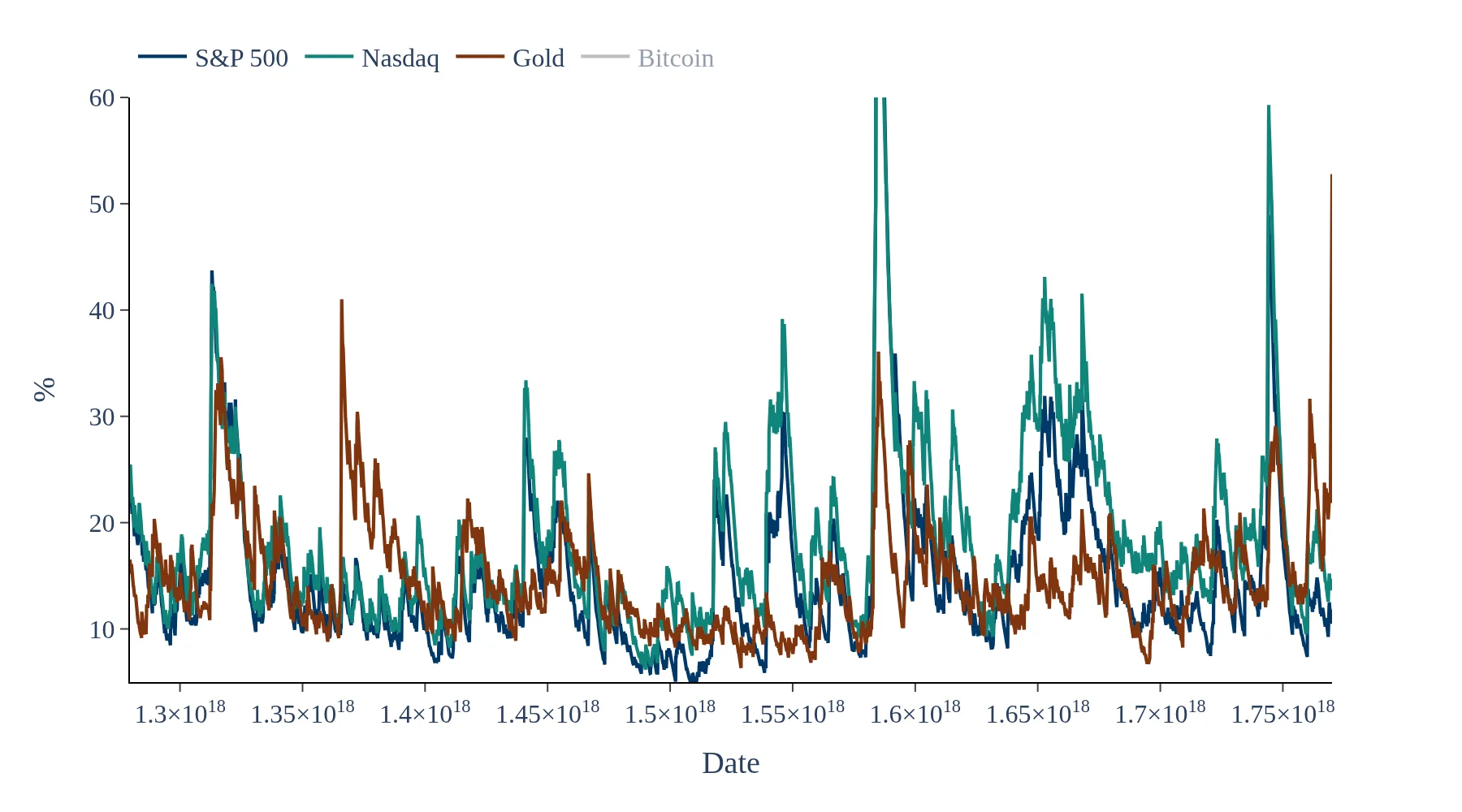

Visualize how realized EWMA volatilities are changing across main asset classes