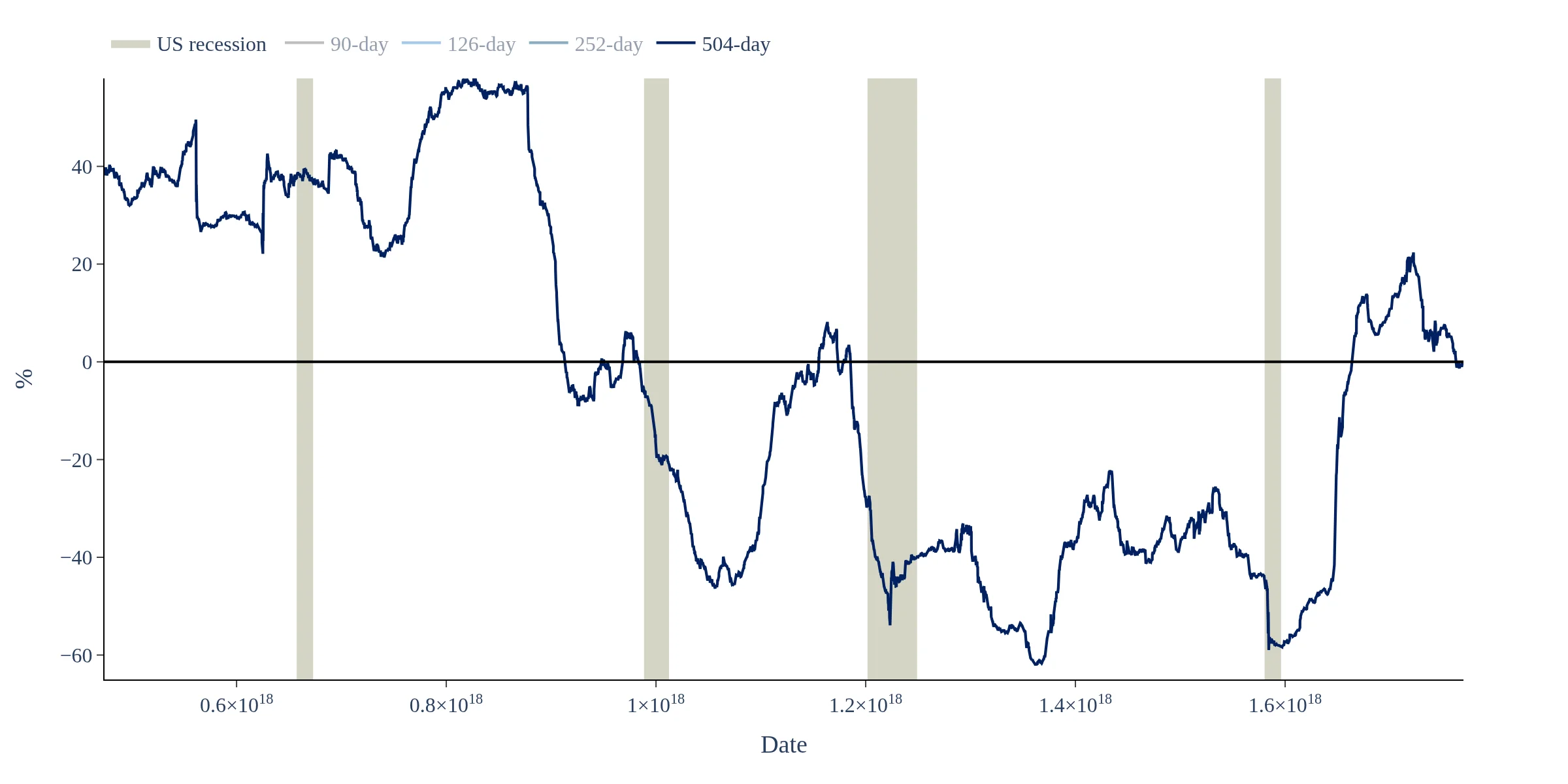

Dashboard consolidating EWMA (Exponentialy Weighted Moving Average) volatilities across the main assets.

The World EWMA Volatilities Monitor utilizes Exponentially Weighted Moving Average (EWMA) methodology to estimate volatility across major global macro assets. By analyzing daily return data with various decay factors, it provides a clear view of market risk, enabling traders and investors to make informed allocation and hedging decisions.

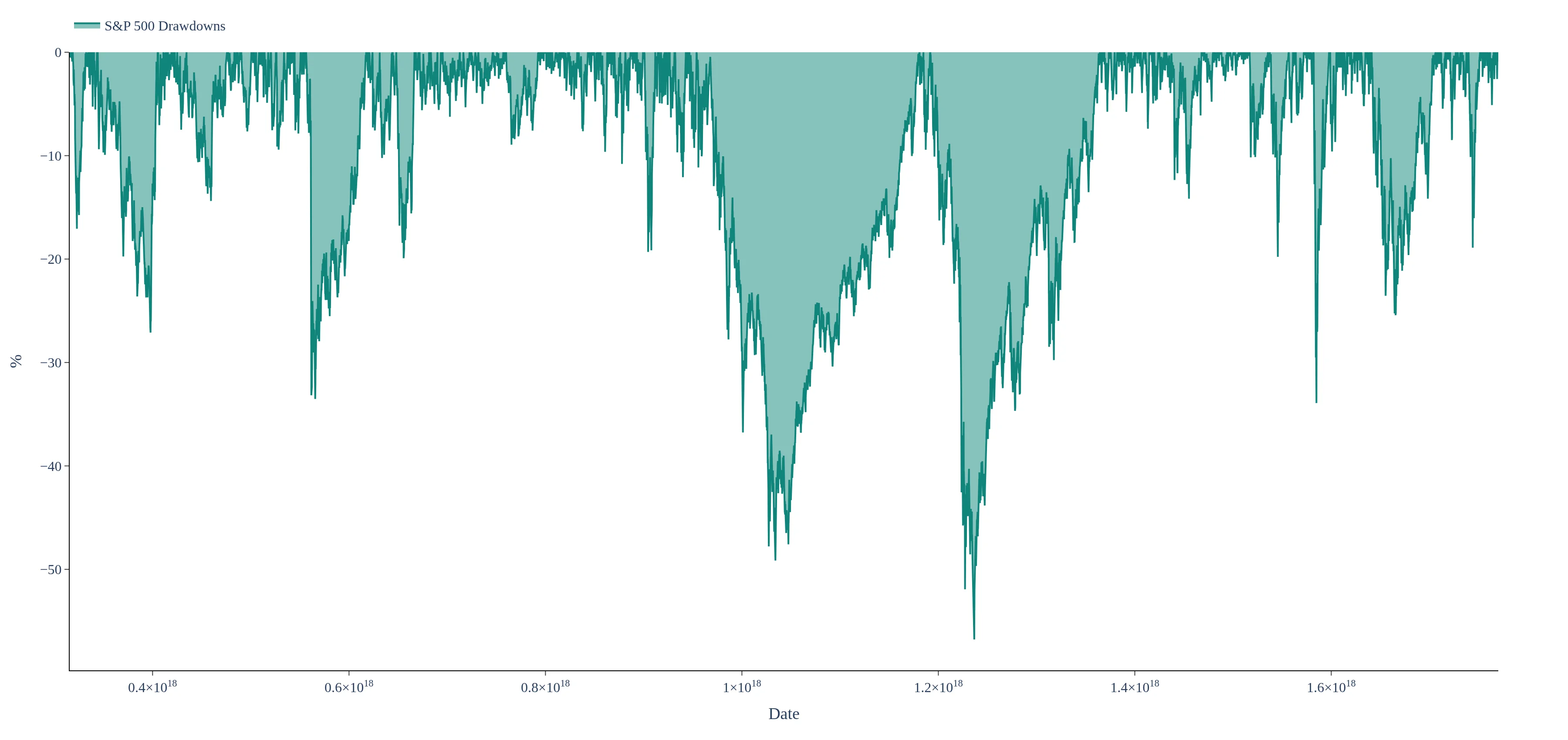

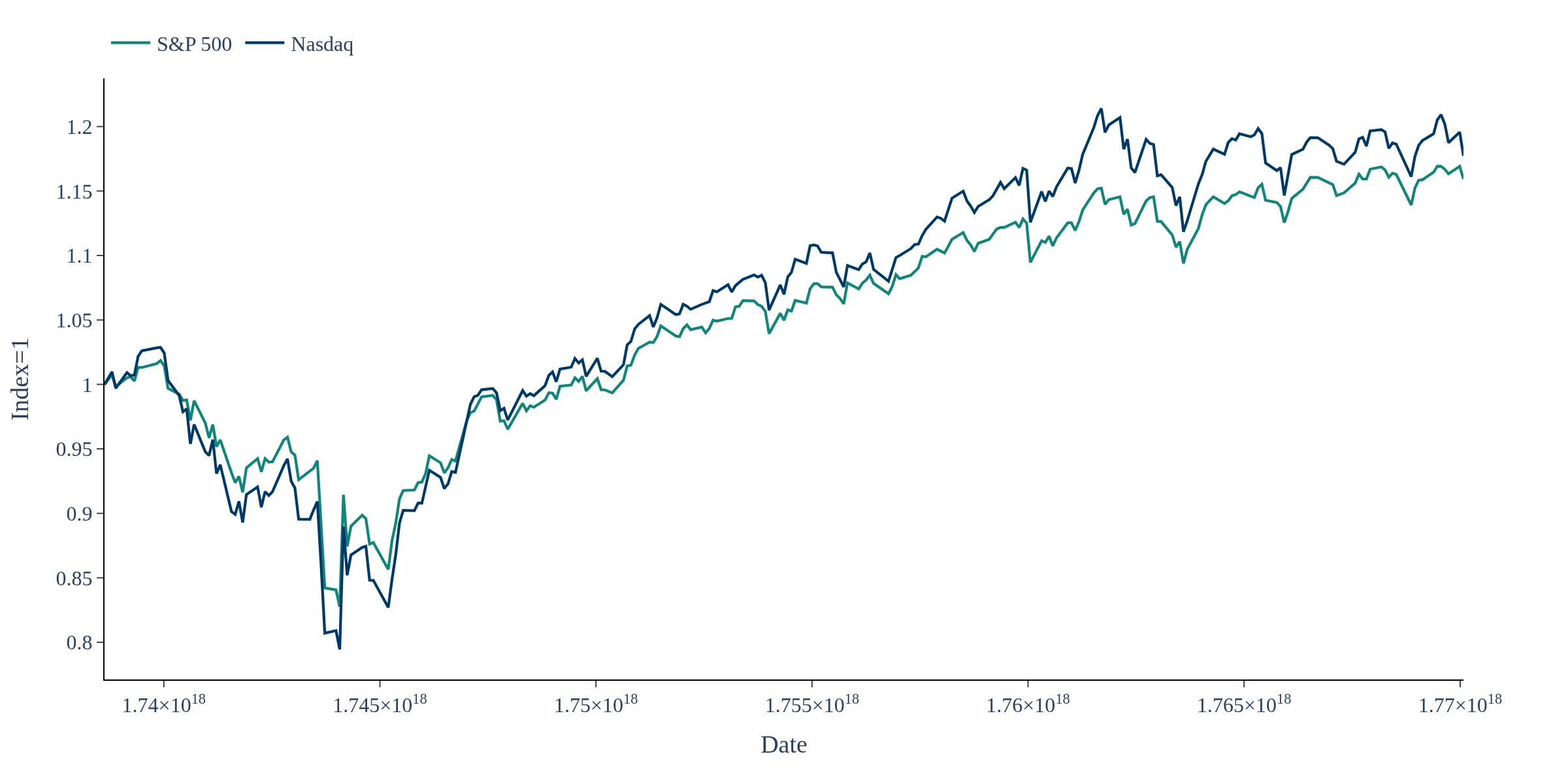

This dashboard analyzes a diverse range of assets, including global equities like the S&P 500 and Nasdaq, commodities such as gold, and cryptocurrencies like Bitcoin. By standardizing volatility results, it allows for effective comparison across different asset classes, enhancing investment analysis.

The World EWMA Volatilities Monitor updates its data on trading days, ensuring that users have access to the most current volatility estimates. This frequent updating is crucial for tracking shifts in market conditions and stress events in financial markets.

This dashboard monitors EWMA (Exponentially Weighted Moving Average) volatility for major global macro assets using daily return data. Volatility is estimated with multiple EWMA decay factors (lambda values) to capture both fast-moving and slow-moving risk regimes. The monitor updates on trading days and standardizes results to make cross-asset volatility comparable over time. Use it to track shifts in market risk, stress events and relative volatility across equities, FX, rates and commodities. The goal is a clear, quantitative view of global risk conditions for allocation and hedging decisions.